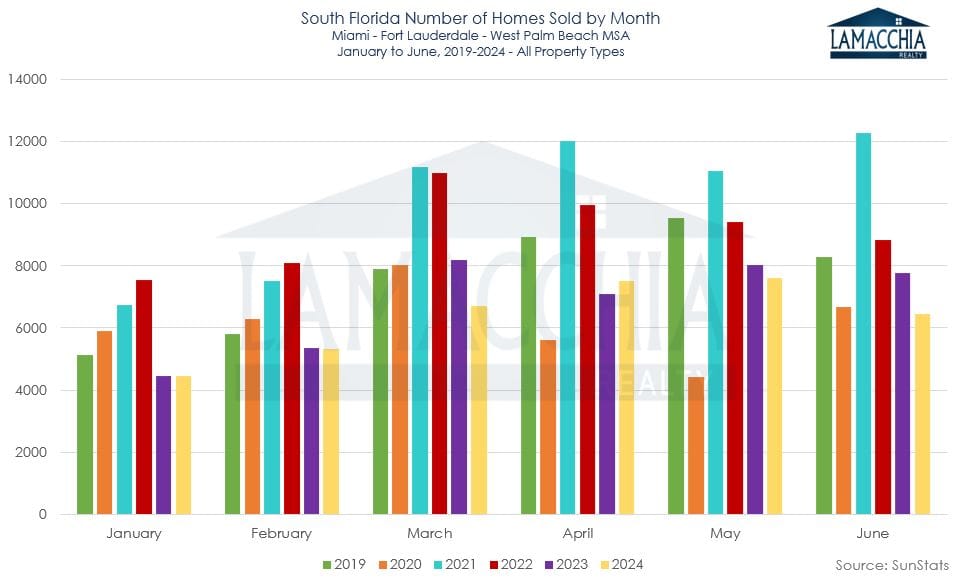

Home sales decreased overall by 7.1% for Miami – Fort Lauderdale – West Palm Beach MSA- there were 40,626 sales in the first part of this year and 37,744 in the same timeframe last year.

- Sales declined for both categories; single families are down 1.3% bringing sales to 18,960 from 19,212. Condo/townhome sales are down 12.3%; there were 21,414 in the first half of last year and 18,784 in the first half of this year.

- While sales dipped slightly in the first half of 2024, the decline was far less pronounced than the steep 25.5% drop experienced during the same period in 2023.

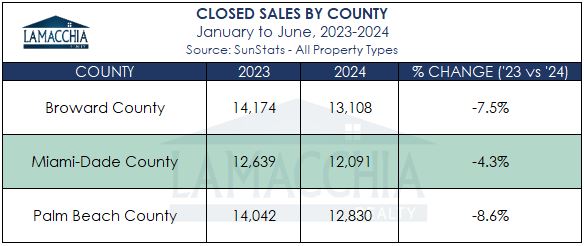

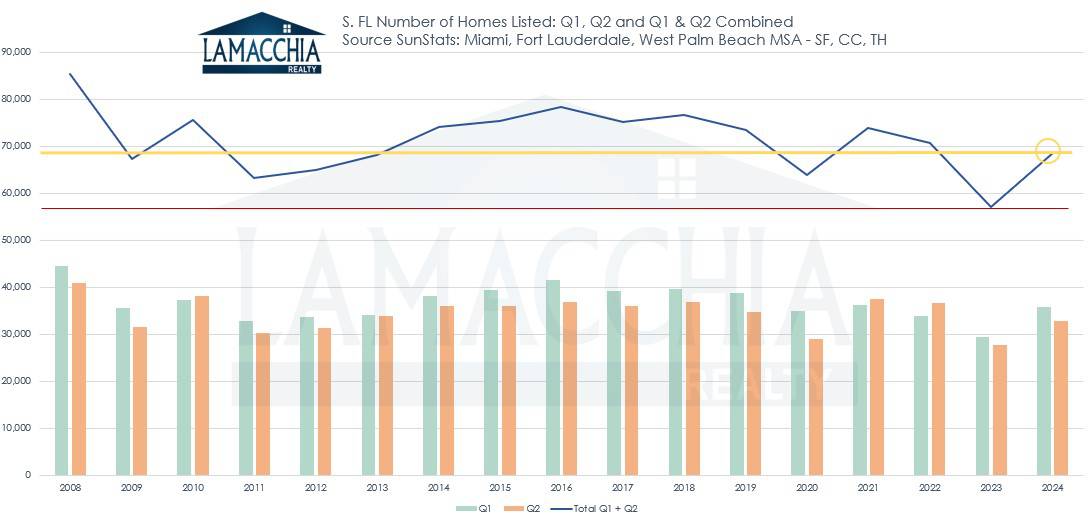

- Active inventory in South Florida has made a giant leap and is back up to

levels from the fall of 2020. Those work-from-anywhere jobs have returned to a form of hybrid or fully back to the office. Some owners have experienced difficulty with rising insurance premiums or condo regulations and assessments. See the yellow line in the graph to the right, and how it’s significantly higher than the last few years.

levels from the fall of 2020. Those work-from-anywhere jobs have returned to a form of hybrid or fully back to the office. Some owners have experienced difficulty with rising insurance premiums or condo regulations and assessments. See the yellow line in the graph to the right, and how it’s significantly higher than the last few years. - Condos & townhomes specifically are being listed faster than they are going under agreement which is greatly contributing to the rise in inventory levels we are currently seeing.

- The bar chart below depicts how sales in 2024 have struggled to keep up with 2023 and, in the end, came up behind.